Dividend Growth in Retirement Portfolios: Maximizing Long-Term Income Stability

Dividend growth investing has been one of my core strategies over the past two decades, helping wealthy families prepare and fund their retirement. In this article, we will cover the ins and outs of utilizing stocks with rising (growing) streams of dividend payments as a way to help fund retirement income.

In the landscape of retirement planning, a strategy gaining traction among investors is focusing on dividend growth within retirement portfolios.

This emphasis on dividend growth is not about chasing high dividend yields per se, but rather seeking out companies with a history and future potential of increasing their dividend payouts.

As retirees look towards their investment income to sustain their lifestyle, a portfolio that can provide growing income streams becomes critically important, especially in the face of inflation and increasing life expectancies.

Incorporating a dividend growth strategy involves selecting stocks that have not only consistently paid dividends but have also shown a pattern of increasing them over time. This approach can potentially offer a two-fold benefit; it provides current income while also reinvesting dividends to buy more shares, which may lead to compounded growth.

Moreover, companies that grow their dividends are often well-established with stable earnings, which can bring an added layer of security to a retirement portfolio. It’s about balancing the need for immediate income with the desire for long-term capital appreciation, which can help maintain and even enhance a retiree’s purchasing power over time.

Key Takeaways

- Dividend growth investing can provide increasing income streams and capital appreciation.

- Selecting stocks with a history of raising dividends can add stability to a retirement portfolio.

- A balance between immediate income and long-term growth is essential in retirement planning.

Understanding Dividend Growth Investing

Dividend Growth Investing is a strategy particularly well-suited to retirement portfolios, as it focuses on companies that not only pay dividends but also consistently increase them over time.

The Role of Dividends in Retirement

Retirement portfolios often rely on stable income streams. Dividends can serve this need, and when reinvested, they compound, boosting the portfolio’s value. Companies that increase their dividends may indicate financial health, which is crucial for long-term income sustainability.

Example:

Here is a chart of Coca-Cola (KO), a well-known dividend-paying stock with a multi-decade history of dividend growth. The purple line represents the day-to-day price of the stock, and the orange line represents the dividend payments.

This chart shows the last 10-year period. You can see how Coca-Cola stock has moved up and down over time, but the dividend payment has seen consistent growth over the years. This is what is known as Dividend Growth Investing.

Investors look to purchase stock in companies with the potential to raise dividends in the future. Then, once they hit retirement age, investors can harvest these dividend payments to fund their retirement income needs (Pretty cool strategy, isn’t it! I certainly think so.)

Dividend Growth Investing Basics

To engage in Dividend Growth Investing, we prioritize companies with a history of raising their dividends. We look for characteristics such as a low payout ratio and strong balance sheets, which are indicative of the ability to sustain and increase dividends.

| Key Factor | Description |

|---|---|

| Payout Ratio | Proportion of earnings paid as dividends. |

| Dividend Yield | Annual dividends divided by the stock price. |

| Dividend Growth Rate | Year-over-year percentage increase in dividends. |

Historical Performance of Dividend-Growing Stocks

Historically, stocks that grow their dividends have outperformed those that do not. They can offer inflation protection as rising dividends can offset the effects of inflation.

| Historical Outcome | Explanation |

|---|---|

| Better Performance During Market Dips | Dividend-growers often provide a buffer in downturns. |

| Superior Long-term Returns | Consistent dividend growth correlates with long-term gains. |

| Inflation Protection | Rising dividends can help maintain purchasing power. |

By focusing on the specifics of Dividend Growth Investing, we aim to curate retirement portfolios that support long-term financial stability and growth.

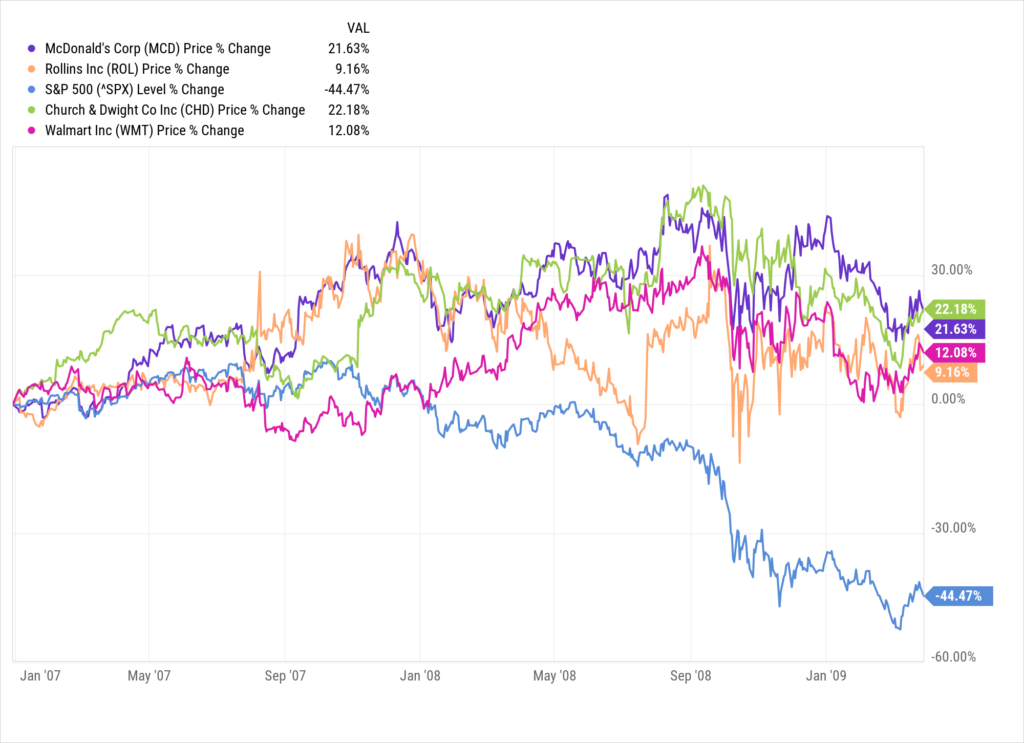

Did You Know

While hundreds of stocks experienced double-digit losses during the 2007-2009 “Great Recession”, a handful of dividend-paying stocks actually made positive returns during this period! While no investment strategy can prevent the loss of money in a down market, history suggests dividend stocks may have an advantage during large market declines.

(see chart below for a few 2007 to March 2009 examples)

Building a Dividend Growth Portfolio

When constructing a retirement portfolio, focusing on stocks that not only pay dividends but also have a history of increasing them over time is vital for sustainable income. We don’t just want current income, we want rising income to help us keep up or even beat inflation.

Selecting the Right Dividend-Growing Stocks

We examine a company’s dividend history to ensure a consistent and rising dividend payout pattern.

Stocks are assessed based on their Dividend Yield and Growth Rate. For instance, we prefer companies with a track record of at least 5 years of consecutive dividend increases.

Key financial ratios like Payout Ratio and Free Cash Flow also guide our selection process, as these metrics indicate the company’s ability to maintain and raise dividends.

| Metric | Why It Matters |

|---|---|

| Dividend Yield | Indicates current income level |

| Growth Rate | Shows historical dividend growth |

| Payout Ratio | Assesses dividend sustainability |

| Free Cash Flow | Measures cash available for dividends |

Diversification Strategies

Diversifying across various sectors and industries is crucial to mitigate risks. We spread our investment across many sectors, including Consumer Goods, Utilities, Healthcare, and more, as different sectors react uniquely to economic cycles.

Within our portfolio, we balance between high-yielding stocks and those with lower yields but higher growth potential. This strategy helps us achieve a blend of immediate income and long-term growth.

Portfolio Allocation Principles

Our allocation approach considers several factors, including individual risk tolerance, time horizon before retirement, and income needs.

Typically, we allocate a higher portion to dividend stocks for those closer to retirement, emphasizing stability and consistent income. For those with a longer time horizon, we may include stocks with the potential for dividend growth, anticipating a rise in yields over time.

| Factor | Allocation Decision Driver |

|---|---|

| Risk Tolerance | Guides balance between stock types |

| Retirement Horizon | Influences growth vs. income focus |

| Income Needs | Determines dividend yield emphasis |

In applying these principles, we continuously review and adjust our portfolio to align with changing market conditions and personal financial objectives.

Maximizing Income Through Dividend Growth

When we approach retirement, ensuring a stable and growing income is paramount. Dividend growth can provide an increasing income stream that outpaces inflation and supports our financial needs through reinvestment strategies, tax-efficient planning, and an understanding of dividend yield and growth rates.

Reinvestment Strategies

Automated Dividend Reinvestment Plans (DRIPs):

- We enroll in a DRIP to automatically reinvest dividends into additional shares, compounding our investments over time.

- This strategy allows us to buy more shares when prices are low, and fewer when prices are high, averaging out the cost.

Selective Reinvestment:

- We carefully select which dividends to reinvest based on company performance and sector stability.

- This requires active monitoring and decision-making to optimize the growth potential of our portfolio.

Tax Considerations for Dividend Income

Retirement Account Placement:

- We hold dividend-paying investments within tax-advantaged accounts (IRAs, 401(k)s) to defer taxes until withdrawal.

Qualified vs. Non-Qualified Dividends:

- We aim to hold stocks long enough for dividends to be considered qualified, benefiting from lower tax rates.

Table: Dividend Tax Rates by Income Bracket

| Income Bracket | Qualified Dividend Tax Rate | Non-Qualified Dividend Tax Rate |

|---|---|---|

| 0-$40,000 | 0% | Ordinary Income Rate |

| $40,001-$250,000 | 15% | Ordinary Income Rate |

| $250,001+ | 20% | Ordinary Income Rate |

*Figures are for illustrative purposes only.

Using Dividend Yield and Growth Rates

Initial Dividend Yield:

- We start with stocks that offer a higher yield without sacrificing quality, as this can provide a significant income base.

Dividend Growth Rate:

- We look for companies with a history of increasing their dividends annually, as this will potentially lead to higher income over time.

- The combination of a respectable starting yield and the potential for dividend growth can significantly enhance the purchasing power of our retirement savings.

Risk Management in Dividend Growth Investing

In managing risks for dividend growth investing, we focus on understanding the inherent risks, actively mitigating specific risks, and continuously monitoring and adjusting our portfolio.

Understanding the Risks

Investing in dividend-growing stocks is not without risks. Market volatility can affect stock prices, while company-specific events can impact dividend payouts.

We identify two primary risks: Market Risk, where the overall market affects our investments, and Company Risk, where the individual company’s performance determines the dividend reliability and growth.

Mitigating Specific Risks

To mitigate these risks, we take a strategic approach. For Market Risk, we diversify across various sectors and geographic locations.

To address Company Risk, we conduct thorough due diligence on a company’s financial health, including its dividend payout ratio and earnings stability.

| Risk Type | Mitigation Strategy |

|---|---|

| Market Risk | Sector diversification, Global diversification |

| Company Risk | Financial analysis, Checking historical dividends |

We also like to mitigate portfolio risk. We do this through proper position sizes and protective stop-loss measures that help us quantify the amount of risk we are willing to take in any single investment position.

We will cover This more advanced technique in future articles and in our advanced courses and newsletter. Be sure to join the Insider Circle to learn more.

Monitoring and Adjusting the Portfolio

We advocate for regular portfolio reviews to ensure alignment with risk tolerance levels and investment goals.

This involves an ongoing assessment of the dividend yield and growth prospects against the backdrop of current economic conditions. Adjustments are made to rebalance or weed out underperforming stocks to maintain a healthy portfolio.

Retirement Planning with Dividend Growth

As we consider the role of dividend growth in retirement planning, we understand its importance in enhancing our income over time and providing potential protection against inflation. The strategies we employ can determine the sustainability and growth of our retirement income.

Integrating Dividend Growth into Retirement Plans

We recognize the necessity of incorporating stocks with a history of increasing dividends into our retirement portfolio.

This practice aims to provide a rising income stream and contribute to the portfolio’s long-term appreciation. The table below highlights key factors when selecting dividend-growing stocks:

| Factor | Description |

|---|---|

| Dividend Yield | We look for a balance between high yield and sustainable growth. |

| Payout Ratio | The proportion of earnings paid as dividends should be manageable. |

| Company Fundamentals | We prioritize companies with strong balance sheets and steady earnings. |

| Sector Diversification | Diversification across sectors minimizes risk and enhances stability. |

Withdrawal Strategies and Sequencing of Returns

We utilize withdrawal strategies that mitigate the risks associated with the sequence of returns. To safeguard our portfolio during market downturns, we might opt to withdraw from the principal less or rely more on the dividend income, allowing the portfolio to recover.

By carefully planning the timing and amount of withdrawals, we aim to preserve our capital for longer durations.

Impact on Overall Retirement Income

Our focus on dividend growth significantly impacts our overall retirement income. With dividends that potentially increase over time, we strive to counteract inflationary pressures.

By reinvesting these dividends during the accumulation phase, we take advantage of compounding, which can substantially impact the total value of our retirement portfolio.

Example For Illustrative Purposes

Here is a 10 year chart showing the S&P 500 Index by [Price Returns only] (purple line) vs. the S&P 500 Index [Total Return] (orange line). This helps to illustrate the difference in price changes only vs. total return which includes the growth and impact of dividends and dividend reinvestment over time.

Frequently Asked Questions

In this section, we address common inquiries regarding the role of dividend growth in retirement portfolios and how it can be optimized for financial stability during retirement.

How can dividends be used to generate income in retirement?

Dividends provide a source of income that can be spent or reinvested. By holding stocks of companies that have a history of paying consistent and growing dividends, retirees can receive regular payments that potentially increase over time, helping to mitigate inflation impacts on purchasing power.

What are the characteristics of a high-yield dividend portfolio suitable for retirees?

A suitable high-yield dividend portfolio often includes stocks with a record of stable and rising dividends and a higher-than-average yield. The companies are typically well-established with strong financials, allowing them to consistently distribute dividends.

What strategies are most effective for building a dividend growth portfolio designed for retirement?

Effective strategies include diversifying across various sectors, investing in companies with a history of dividend increases, and considering the dividend payout ratio to assess sustainability. A focus on dividend aristocrats—companies with a history of increasing dividends for at least 25 consecutive years—may also be beneficial.

How does one construct a balanced retirement portfolio that includes a mix of dividend stocks and other assets?

Constructing a balanced portfolio entails allocating investments across different asset classes, including dividend stocks, bonds, and potentially other income-generating assets such as real estate. This helps to manage risk while aiming for a steady income stream.

What are the benefits and drawbacks of relying solely on dividend-paying stocks during retirement?

The benefits include the potential for a reliable and growing income stream and favorable tax treatment for qualified dividends. The drawbacks are the risks associated with stock market volatility and the possibility of dividend cuts during economic downturns.

Can you achieve financial independence and retire early (FIRE) primarily through dividend growth investing?

Achieving FIRE through dividend growth investing may be possible by accumulating a large portfolio of dividend-paying stocks that can generate sufficient income to cover expenses. However, it requires prudent planning and substantial investment to reach the necessary portfolio size.